The Containerised DSP: Why Fifteen Years of Programmatic Orthodoxy Just Ended

Microsoft Just Shut Down Its DSP. Here's What Replaces It.

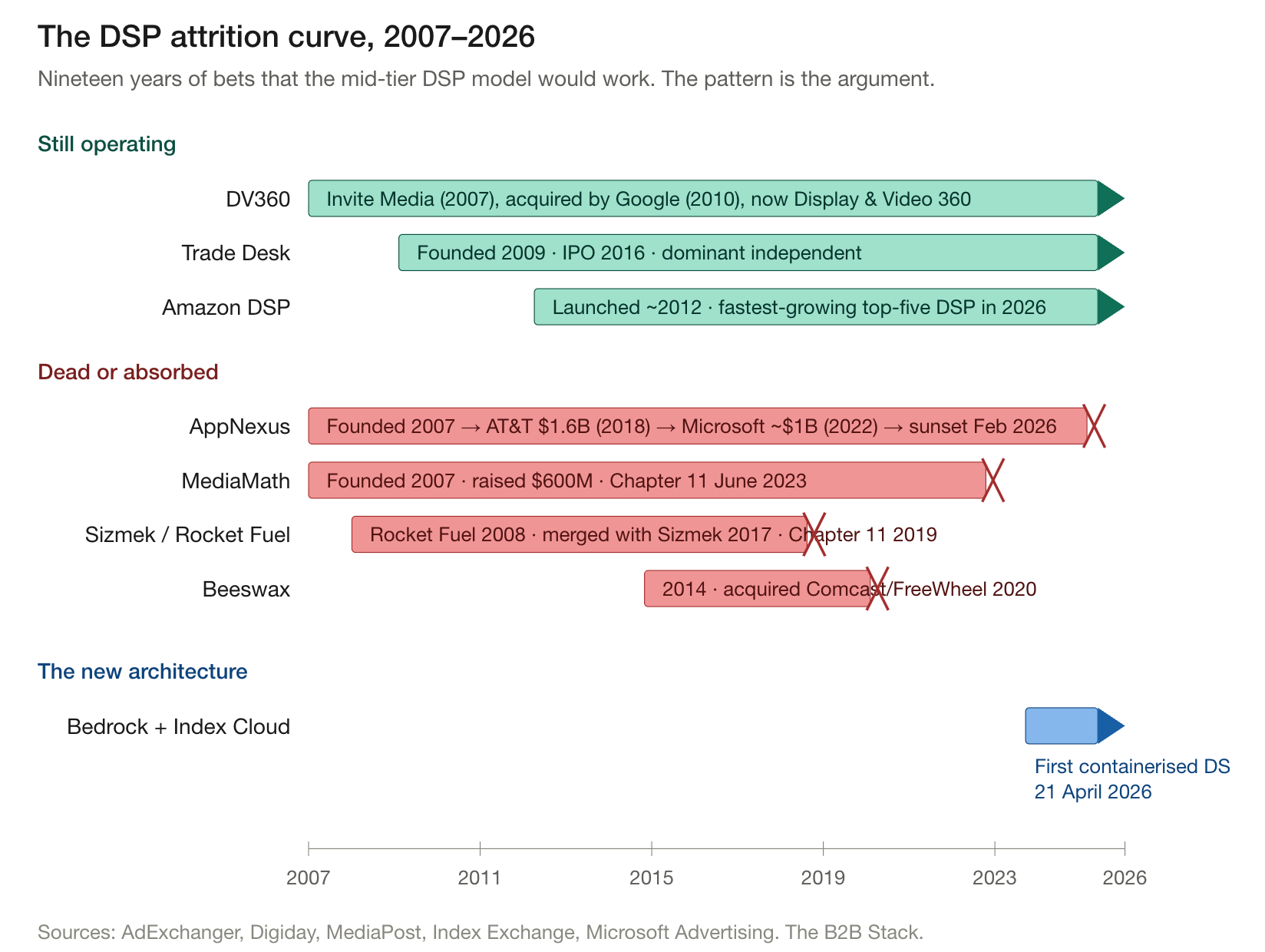

On the 28th of February 2026, Microsoft quietly switched off the DSP it had bought from AT&T four years earlier for around a billion dollars. The platform had previously been Xandr, and before that AppNexus — for more than a decade one of the most respected names in programmatic, the open web’s most credible non-Google challenger, the centre of gravity of the AT&T adtech ambition that valued it at $1.6 billion in 2018. By 2026 it was gone. Microsoft kept the supply side (Monetize) and the curation layer (Curate). The buy side it simply stopped supporting. When I entered Adtech in the late noughies, AppNexus was the poster child of innovation, it was everything which was great about adtech - category creating even - so on a personal level its demise left a gap.

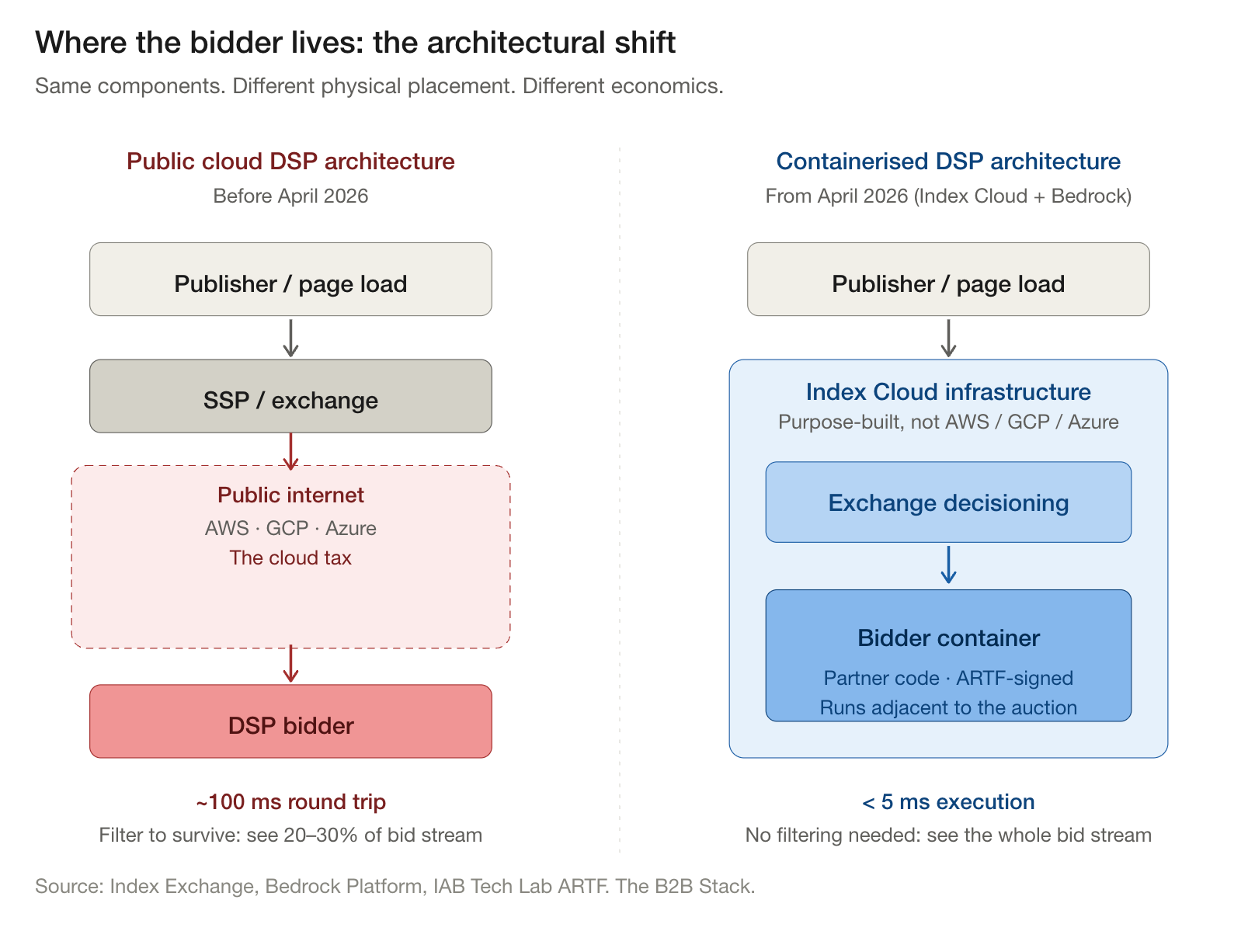

Two months later, on the 21st of April, Index Exchange, a leading sell side platform which has stayed true to its routes, and a two-year-old London-headquartered DSP called Bedrock Platform went live with the open web’s first containerised demand-side platform. Bedrock’s bidder, its full decisioning logic, was lifted out of public cloud infrastructure and dropped inside Index’s own data centres. The execution window for a bid decision collapsed to under five milliseconds. If you have spent any time at all around programmatic advertising, this is genuinely astonishingly fast and as we will come to shortly, it opens a lot of opportunities to re-use the time saving.

A few weeks after that, Andrew Casale, the President and CEO of Index Exchange, sat down with First Party Capital for an episode of The FPC Podcast and tied the threads together. The headline soundbite — “we are at the outset of a structural shift in programmatic” — is the sort of thing exchange CEOs say at trade shows. The substance underneath it is not. The two announcements ten weeks apart, taken together, mark the end of an orthodoxy that has shaped fifteen years of investment, M&A and product strategy across adtech. And they matter more, for structural reasons, to B2B programmatic than to almost any other corner of the open web.

If you have ever tried to find six chief financial officers across two hundred named accounts in a single quarter, you already understand why.

What you’ll learn in this article

Why for fifteen years every serious adtech business felt commercially obliged to be inside the DSP layer, and why that orthodoxy quietly died this spring

What “audience containerisation” actually means in plain English, and why moving the decisioning layer inside the exchange is structurally different from anything that came before

How the cost of looking at the bid stream became the dominant constraint on B2B targeting, and why mid-tier DSPs were always going to lose this fight on cost economics alone - this is why I always argued that B2B should not have its own bidding tech and should lean on the roadmaps of the giants.

Why live sports on connected TV exposed the queries-per-second problem in public, and why this matters more for needle-in-haystack B2B audiences than for the broad-reach buyers who have historically set platform agendas

How a five-millisecond decisioning window unlocks reactive, signal-driven creative — including person-level buying committee targeting that has been theoretical for a decade

What B2B marketing teams should actually do differently in the next twelve months as this shift compounds

Fifteen years of the wrong orthodoxy

For most of the last decade and a half, the unspoken rule of adtech strategy was simple: if you wanted to be a serious player on the open web, you needed exposure to the demand-side platform layer.

The reasoning, on a whiteboard, looked airtight. The DSP was where the bidding decision happened, where the data lived, where the optimisation models ran, where the margin sat. Own the DSP, or own a meaningful piece of one, and you owned the customer relationship, the bid economics, the integration roadmap, the strategic floor. Lose it and you were renting from someone else’s roadmap forever.

The agency holding groups built their version of this thesis through trading desks. WPP launched Xaxis in 2011, assembling it on the bones of GroupM’s earlier programmatic operations and the 2007 acquisition of 24/7 Real Media. Publicis had VivaKi Audience on Demand. IPG had Cadreon. Omnicom had Accuen. Havas built Affiperf. Dentsu had Amnet. By the mid-2010s most of the holdco trading desks had quietly decommissioned the in-house DSP layer and switched to running through external DSPs — Xaxis itself publicly mothballed its own DSP in 2013, explicitly because the technology had commoditised. They kept the audience layers, the supply relationships, the trading desks themselves. They gave up on operating the actual bidder.

The pure-play DSPs followed a steeper version of the same arc. MediaMath raised about $600 million across its life, hit a peak valuation north of a billion, and filed for Chapter 11 in June 2023 owing somewhere between $100 million and $500 million to a creditor list that read like a roll call of the supply side. Sizmek absorbed Rocket Fuel in 2017 and went into Chapter 11 in 2019; Amazon picked up parts. Verizon paid $9 billion combined for AOL and Yahoo, merged them into Oath, wrote down $4.6 billion, and sold the lot to Apollo for $5 billion in 2021, half what it paid in. Beeswax was bought by Comcast and absorbed into FreeWheel. Basis (formerly Centro) remains a useful boutique alternative but isn’t competing at Tier-1 scale.

And then there was AppNexus. AT&T paid $1.6 billion for it in 2018, renamed it Xandr, sold it to Microsoft for around a billion in 2022, and watched Microsoft announce its closure in May 2025 before formally sunsetting the platform on the 28th of February this year. Microsoft, the second most valuable company in the world, with arguably the deepest cloud and AI moat in technology, could not make the mid-tier DSP economics work. The end state, in 2026, is that two general-purpose DSPs have meaningful share of B2B-relevant open web buying — The Trade Desk and Google’s DV360, with Amazon DSP growing fast in retail-adjacent buying and a long tail of specialist platforms operating in pockets. Everybody else lost. I was one of them with my first adtech business, PowerLinks, which didn’t make it in the world of native bidding.

The reason they lost is not ideological, and it is not operational. It is arithmetic.

The reason the orthodoxy held: hundreds of billions of auctions a day

A bid request is a network event. An SSP serialises a JSON payload describing an impression opportunity, sends it across the public internet to one or more DSPs, waits for a response inside a strict timeout window — typically 100 to 200 milliseconds on the DSP side, depending on the integration — then resolves the auction. At the open web’s current scale, the total volume of unique impression auctions runs into the hundreds of billions per day, and nets out at around 700b auctions when we make the best possible efforts to remove the hugely duplicative nature of oRTB. RTB bid request volume, counted across the duplication created by header bidding, runs into the trillions. The same impression, on the same page, at the same moment, exposed simultaneously through fifty-plus supply paths to the same buyer pool.

Each loop costs money. Compute on the DSP side to deserialise the request, run model inference, decide whether to bid and at what price, serialise the response. Egress bandwidth, often the dominant line item, billed by the hyperscalers at a premium. Storage and retrieval for the contextual signals, user identifiers, audience segments and frequency caps the bidder needs. At hundreds of millions of requests a day per DSP, the marginal cost of merely seeing the bid stream — before any working media is spent — stacks up to seven or eight figures a month. When we set out to build FunnelFuel, a B2B programmatic managed service, we decided this money would be much better invested in upgrading the best of the incumbent stack, and to borrow a phrase I over-use, we did not want to rebuild the wheel. This tech is commodity, and the cloud computing cost of listening to B2B volumes would be hugely wasteful in every sense possible, whilst adding no value. This is why the DSP 2.0 won’t live at the end of a full unthrottled bidstream, and why containerising it is so important moving forward.

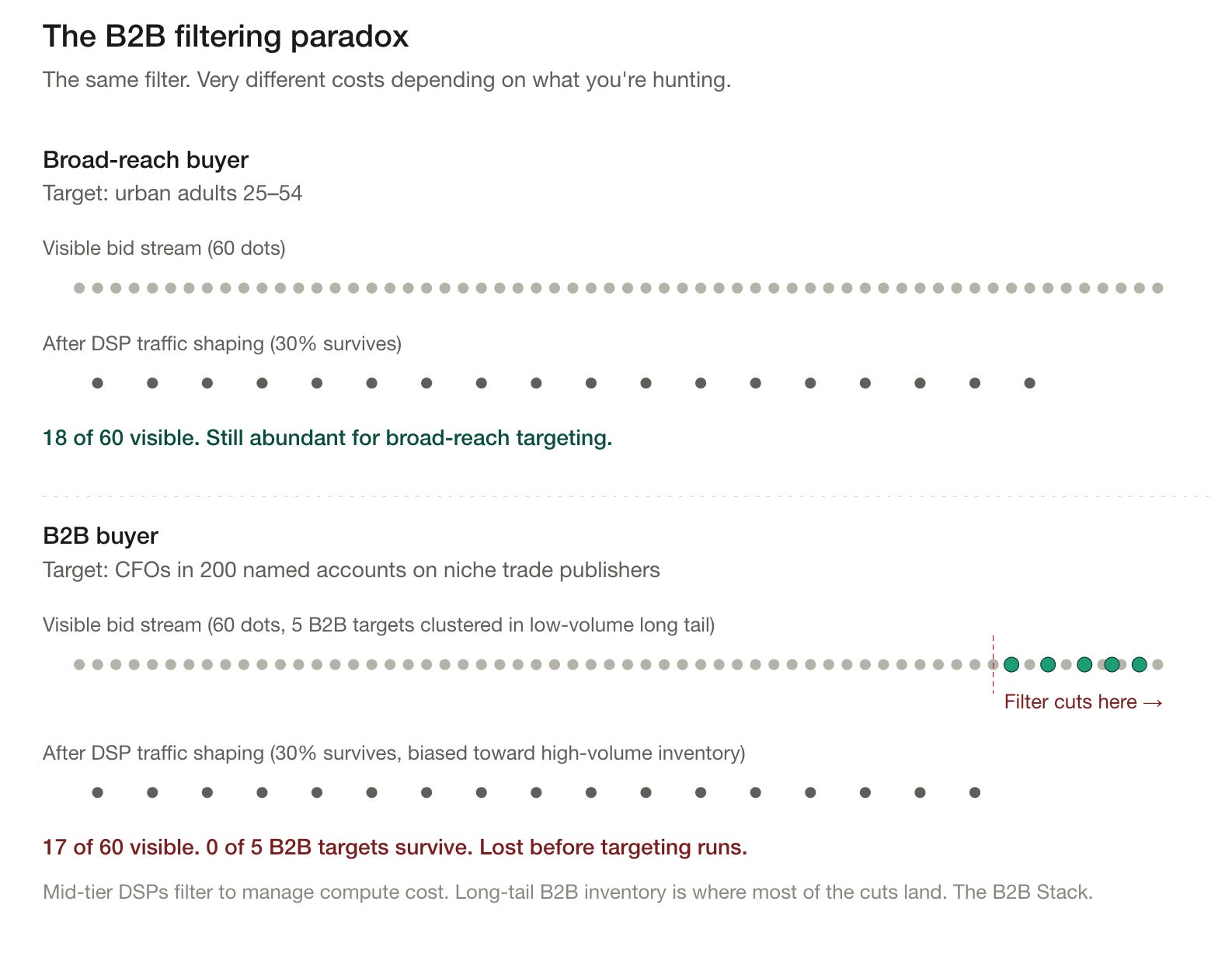

As header bidding exploded, the DSP responded rationally by filtering. Accept the share of inbound traffic that traffic shaping logic predicts is most likely to convert into winning bids, ignore the rest. Industry analyses routinely place the surviving share at somewhere between 20 and 30 per cent of available impressions.

If you are in niche audiences, like B2B, read that last line again. That is huge. Put another way - 70-80% of all B2B audiences are getting lost to bid throttling, indiscreetly, and forcing many programmatic teams to chase the scale into consumer environments, like broad content sites and gaming. This is the whole containerised audience thesis in one line - would you like to see ALL of your audience or 20-30% of it?

That QPS filter isn’t science, acknowledged by Andrew Casale on the FPC podcast linked above. It’s a heuristic for survival, calibrated on volumetric assumptions about which auctions are most likely to clear. It is, in plain language, an educated guess about which inventory matters, made at scale, with the cost of being wrong borne by the advertiser rather than the platform. In B2C, its tolerable, in B2B is is not.

For broad-reach advertisers — the people targeting urban adults 25 to 54, or seasonal car buyers, or recently engaged mortgage shoppers — this guesswork is mostly invisible. The filtered-out 70 per cent contained some signal, but the surviving 30 per cent still represents hundreds of millions of impressions, more than enough to deliver the campaign. The cost of filtering doesn’t show up in performance reports because the targets are so abundant.

For B2B, the cost is structural. We’re not buying urban adults. We’re hunting Chief Financial Officers and Chief Product Officers and IT decision-makers in specific named accounts in specific regions, often in pursuit of pipeline progression rather than top-of-funnel reach. A target account list might be two hundred companies. The buying committee inside each is six to twelve people. That’s a universe of maybe two to three thousand individuals you actually want to reach in any given quarter. Every impression discarded by upstream traffic shaping is potentially one of yours. The approach of trying to fix this by building a bidder is laughable today, but equally the opportunity to find these people in the worlds best supply pools is not.

I actually think the problem is even worse for B2B DSP buyers then the headline filtering implies, because the shaping is biased against B2B inventory before any of your targeting logic runs. Niche trade publications, technical content, finance and engineering media, vertical newsletters — the long-tail open web where B2B audiences actually spend time — are exactly the publishers whose auction volume is lowest, whose CPMs are highest, and whose impression patterns look “unprofitable” to a model optimised for broad-reach efficiency. Coca Cola and McDonalds do not want to pay the premium to reach crn.com, and they outspend Dell who will pay it. The DSP filters them out for reasons that have nothing to do with your campaign and everything to do with its own cost structure, and the democratic process of finding the best inventory for the most buyers.

Casale, on the FPC episode and earlier at the IAB Annual Leadership Meeting in February, called this dynamic an “invisible cloud tax on adtech.” That’s polite framing. A more accurate description is that the cost of looking at the open web became the dominant constraint on who could compete, and that constraint silently mortgaged the open programmatic ecosystem to the hyperscalers. Every dollar of media planning energy spent worrying about supply-path optimisation in the last five years was downstream of a structural problem that nobody could solve at the DSP layer because the cost lived at the infrastructure layer.

Live sports on CTV broke the model in public

For most of the open web’s history, auction volume was relatively predictable. Display impressions distributed across millions of pages, served in a smooth roll throughout the day, with broad geographic and temporal patterns that allowed for reasonable forecasting. A DSP could model its traffic shaping logic against a stable distribution.

Connected television changed that. Not television itself, the IAB has been forecasting CTV for years, but specifically live sports on CTV. A Champions League final, an NFL Sunday window, a Formula One race, a Premier League slot: millions of synchronised viewers, ad pods opening simultaneously, demand spiking ten to twenty times baseline volume in single-digit seconds, then collapsing. The bid stream lumpiness CTV creates is fundamentally different from the smooth distribution of the historical open web. It exposed the cracks. It exploded the model

Casale spent a meaningful chunk of the FPC conversation on the queries-per-second pressure live sports creates. Every DSP needs to be present in those windows because that’s where the demand is. Every DSP times out under load because the QPS spike outstrips their provisioned capacity or their filtering evens out the spikes entirely, missing the structural moments in ad breaks around big cultural events. Every DSP ends up bidding on a partial view of the most commercially important inventory of the year, on rapidly changing contextual signal — score, momentum, the team competing, who scored last, who’s about to commercial-break — with traffic shaping logic calibrated for a market state that no longer exists by the time the model fires.

The upcoming World Cup is going to expose this like never before, the first time the biggest global sporting event hits with CTV reaching greater scale maturity.

The most-cited proof point of the cost of solving this properly was published by Index Exchange and FreeWheel in March — an A+E Global Media case study documenting an 84 per cent reduction in inbound ad server requests, a 39 per cent rise in impressions, and a 19 per cent lift in ad spend for podded inventory after moving from slot-level to pod-level auctions through OpenRTB 2.6. The architecture is technically distinct from containerisation. The principle is the same: move the decisioning closer to the impression, and the wastage in the middle layer evaporates.

For B2B advertisers this matters in two ways. The obvious one is that CTV is now a real B2B channel — but only useful if your buying platform can do impression-level decisioning that ties to an account list, and only economic if the cost of doing that decisioning at the necessary granularity is reasonable. The less obvious one is that live sports was the canary. The same architectural problem that breaks in public during a Champions League final is breaking continuously, less visibly, across the long-tail B2B inventory that mid-tier DSPs were never able to fully participate in. The Microsoft Xandr shutdown is the upstream signal: the company with the deepest pockets in adtech outside of Google decided the cost curve was unfixable.

Containerisation: what it actually means

Strip away the marketing language and the architecture is straightforward.

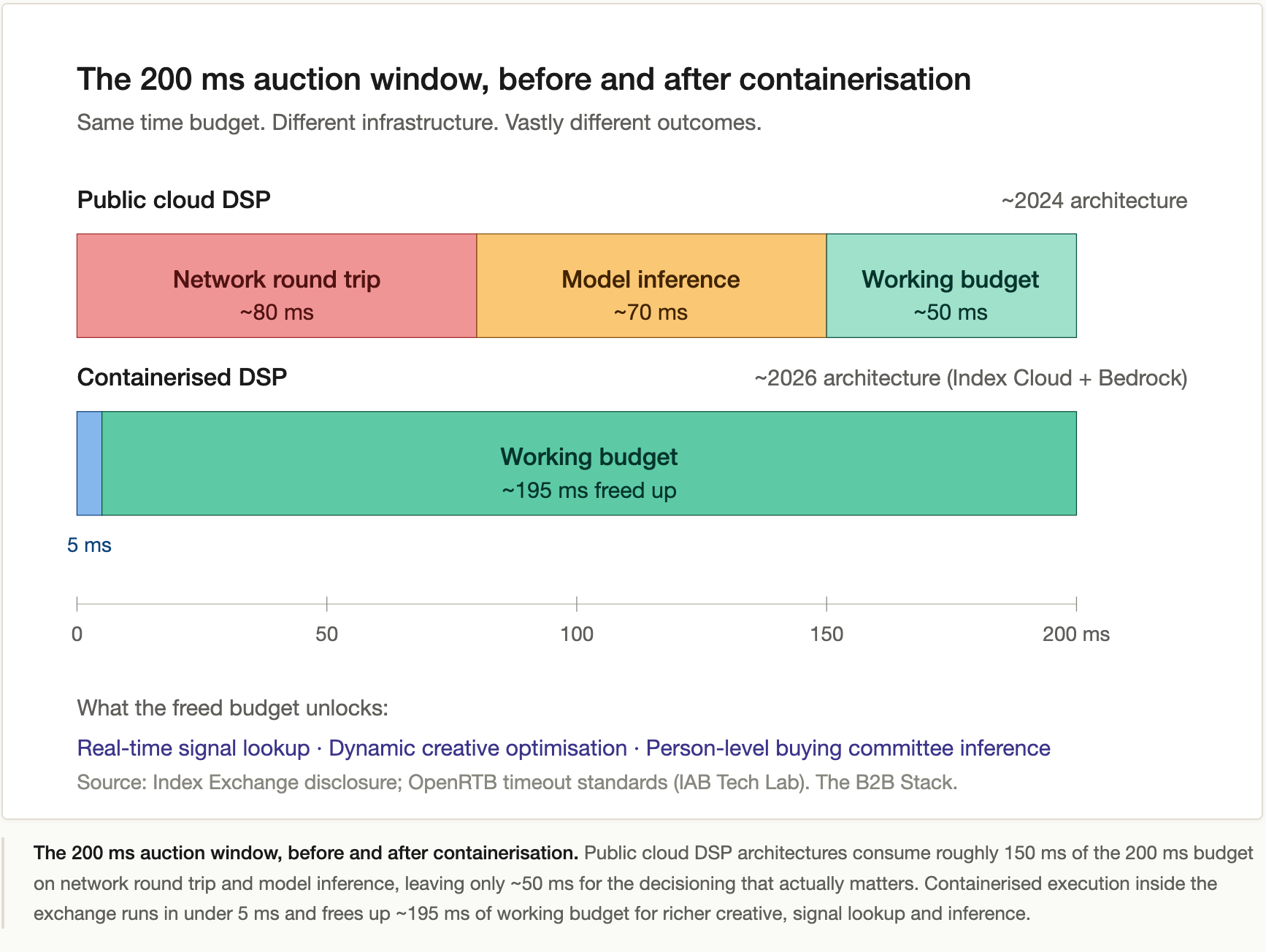

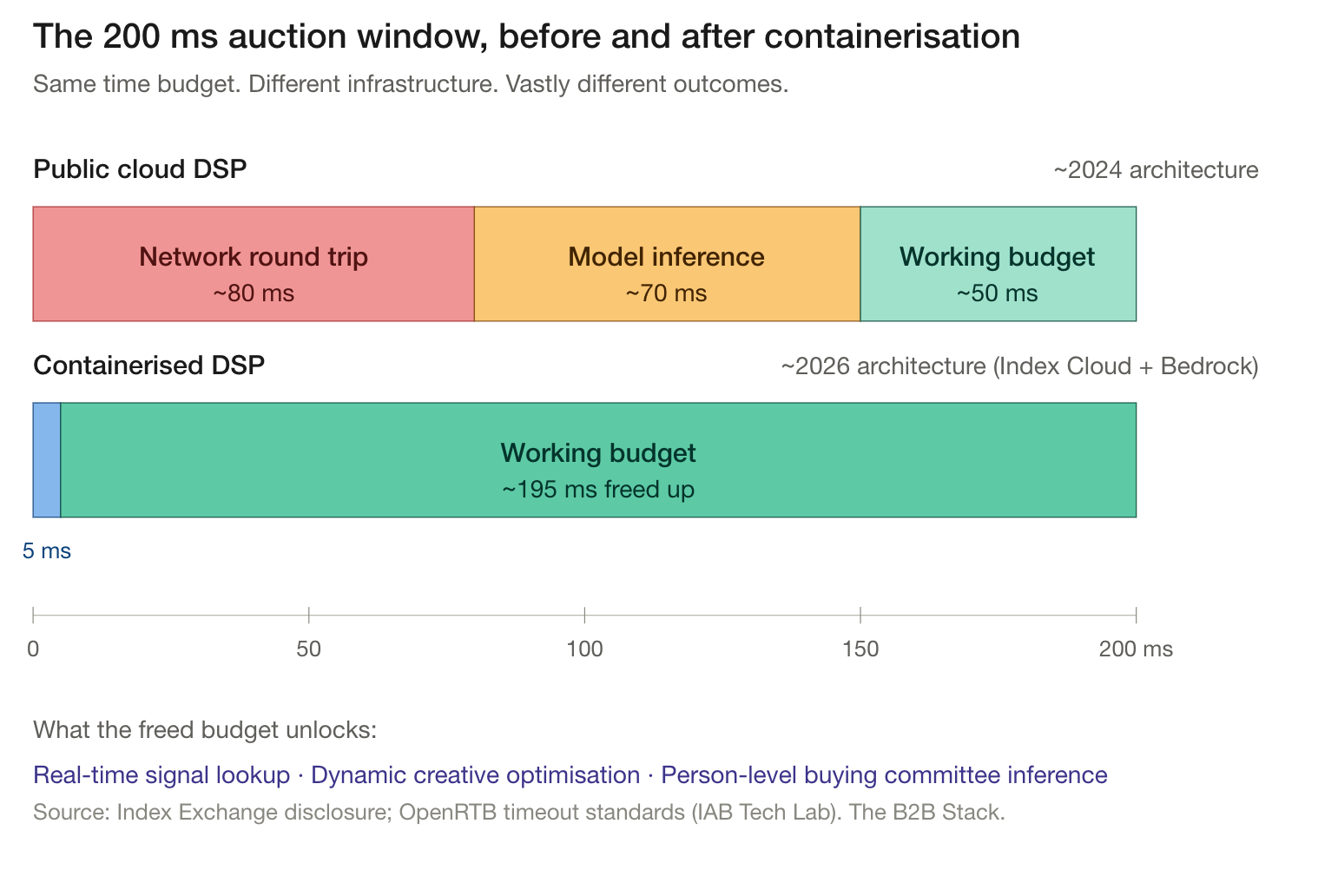

Historically, the DSP’s bidder lived in AWS or GCP, typically tens to low hundreds of milliseconds of network round-trip latency away from the SSP. A DSP-side bid response budget of 100 to 200 milliseconds is industry standard. Of that budget, network round-trip latency between the SSP and the DSP’s cloud region can eat anywhere from 30 to 100 milliseconds depending on geography. By the time the request has arrived, been deserialised, evaluated, the bid serialised and returned, the bidder has perhaps 50 to 100 milliseconds of working budget for model inference, audience lookup, frequency capping, creative selection and pricing. That budget has been the binding constraint on what a DSP can actually do per impression for the last decade.

Containerisation puts the bidder’s decisioning code, packaged as a portable, cryptographically signed container, inside the exchange’s own infrastructure. Index Cloud doesn’t run on AWS, GCP or Azure. It’s purpose-built, sitting next to the exchange’s own auction logic. When an impression becomes available, the partner’s container receives the impression-level signals, applies its own logic, and returns a decision, all before the bid request is constructed for downstream DSPs. The entire execution window, per Index’s own disclosure, runs in under five milliseconds.

That changes the maths in three ways that matter.

First, the DSP can see and bid on a materially larger share of the bid stream. Filtering for survival becomes unnecessary because the infrastructure cost of looking is no longer the binding constraint. A small, focused DSP can now listen to substantially more of the open internet than it could when it was paying hyperscaler egress fees for the privilege.

Second, round-trip latency collapses. The hundred-millisecond budget historically consumed by network plumbing is freed up. That budget can now be redeployed into model inference, creative decisioning, dynamic optimisation, signal lookups — all the things B2B advertisers have been told were possible for a decade and which never quite worked at scale because the latency budget killed them.

Third, infrastructure cost decouples from market access. This is the killer point. Until April, the rule was: the more of the open web you wanted to see, the more compute you needed to buy. Scale was a function of capital. Now it isn’t. As Bedrock’s Shane Shevlin put it in the announcement, the goal is to “compete on decisioning and performance rather than infrastructure.”

The standardisation layer that makes this interoperable rather than a closed Index thing is the Agentic Real-Time Framework, published by IAB Tech Lab earlier in 2026 with Index as one of the pioneering contributors. ARTF formalises how containers plug into exchange infrastructure, how the cryptographic signing works, how the isolation between partner code and exchange code is preserved. It’s the protocol layer that prevents this from becoming a single-vendor walled garden, and its design has been shaped by live deployments rather than committee whiteboarding. ARTF sits inside IAB Tech Lab’s broader agentic initiative AAMP — the agentic ad management protocol layer — which is the open web’s serious attempt to position for an era where AI buying agents transact alongside, and eventually instead of, human-configured campaigns.

The first wave of partners running on Index Cloud is publicly listed: Bedrock Platform on the DSP side, then Chalice AI, inPowered AI, Nano Interactive and FunnelFuel Navigator on the data and decisioning side. (Disclosure that informs my read: Navigator is the audience and decisioning layer FunnelFuel operates, and I’ve had a close view of this architecture from before the public launch which will come in Q4.) That list will grow. ARTF will iterate. But the structural point is that the era of having to be hyperscaler-funded to listen to the whole internet is over. As Digiday reported last week, agencies — including those that historically would have run everything through Tier-1 DSPs — are themselves now leaning toward models that put them closer to supply and further from infrastructure rent extraction.

What this unlocks for B2B specifically

Three things, in order of how immediately they matter.

Listening at scale becomes economically possible for specialists. For years, the credibility argument for using a Tier-1 DSP on B2B campaigns was that they were the only platforms that could see the long-tail inventory at the scale a needle-in-haystack audience required. That was true. It isn’t necessarily true any more. A focused, B2B-native bidder running inside Index Cloud can listen to as much of the open web as a Tier-1 — at a fraction of the infrastructure cost. The economic argument for using a generalist platform with B2B grafted on top weakens correspondingly. Specialist managed-service operators in B2B have a structurally lower floor on what they need to charge to compete on infrastructure parity. Margin that previously had to fund hyperscaler egress fees can be redirected into the things that actually matter for B2B — first-party data integration, account-level measurement, account-graph maintenance, creative iteration.

Dynamic creative optimisation that actually works. This is the practical unlock. The hundred milliseconds freed up by collapsing round-trip latency is enough to run real creative decisioning at impression time. Reactive creative tied to live signals is no longer a pitch-deck capability. A B2B sponsor of a Formula One team — Hewlett Packard Enterprise sponsors Mercedes, Oracle sponsors Red Bull, AWS sponsors Ferrari — can now plausibly run creative that reflects the live state of a race in the moment, on impressions served to in-market IT decision-makers in named target accounts watching CTV coverage in target territories. The same goes for tying creative to live financial signals, earnings windows, conference moments, M&A news, product launches. None of this was meaningfully deliverable a year ago because the maths wasn’t there. The maths is there now.

Person-level buying committee creative becomes viable. This is the area I find most interesting personally. The decade-long pitch in B2B has been “right person, right account, right moment, right message.” What has actually happened, in most stacks I’ve seen, is account-level targeting with one or two creative variants tested at the campaign level. The constraint was never the data — we have psychographic signal from past content engagement, content syndication download history, intent topic clusters from Bombora (whose raw-signal partnership architecture is itself the closest precedent for what containerisation now enables at the bid layer), email engagement, audio and podcast listening signal, CTV viewing data, first-party web analytics. The constraint was that you couldn’t bring all of that together inside the bidding window and personalise creative at the individual-within-account level fast enough to fit a 200-millisecond auction. Five-millisecond decisioning windows change that. Signal-based inference around person-level buying committee creative targeting goes from theoretical to operationally plausible, and that is the next real frontier in B2B media — not just better targeting, but creative that actually reflects what each individual member of a buying committee responds to.

What this doesn’t change

A few honesty notes, because the editorial standard on this newsletter is not to oversell.

Containerisation doesn’t fix the walled gardens. Meta, YouTube, Amazon, TikTok still represent more than half of digital ad spend globally, and none of them are about to expose impression-level decisioning to third-party bidders. The open web’s economics improve markedly. The walled gardens’ don’t.

It doesn’t fix B2B identity. Post-cookie, the open web still relies on a fragmented combination of Unified ID 2.0, RampID, Google’s Privacy Sandbox, contextual signals and first-party data partnerships. Containerisation gives those identity systems a better operating environment, but it doesn’t resolve the underlying fragmentation.

It doesn’t fix measurement. Account-level attribution on the open web is still patchy. CFOs will still ask awkward questions about programmatic margin and working media ratios. None of that goes away because the bidder moved closer to the exchange.

And it doesn’t make Microsoft’s decision look smart in hindsight, or stupid. Microsoft’s bet — that the future of advertising is AI-mediated conversational surfaces inside the walled garden it’s building with OpenAI — is a coherent bet about where the spend will go. Index and Bedrock’s bet is a coherent bet that the open web will survive as the primary venue for advertiser-controlled reach, provided someone rebuilds its economics. Both can be right. They aren’t competing for the same future.

What containerisation does do, structurally, is lower the cost of operating a credible specialist platform on the open web by an order of magnitude — which is the precondition for a wave of innovation in B2B-specific decisioning, creative and measurement that the existing cost curve had been suppressing.

What B2B marketing teams should do about it in the next twelve months

Five things, in rough order of how soon you should be doing them.

First, stop asking your DSP partner what their “access” to the bid stream is, and start asking what their architecture is. Where does the decisioning run? Is the bidder hosted on a public cloud, an exchange-side container, or a hybrid? What percentage of available bid requests does the platform evaluate end to end, and how is that share changing? The vendors who can’t answer those questions clearly are the vendors who will be structurally disadvantaged over the next eighteen months.

Second, audit how your audience and signal partners are deploying their data. There are now three distinct architectures: data applied at the bidder (the historical model, with all the latency tax that implies), data applied in transit through curation (the deal ID model that has become standard in 2024-25), and data applied containerised inside the exchange (the new pattern). The performance gap between these three is about to widen. If you are paying a premium for third-party data, you should know which architecture it is running through.

Third, plan for the creative shift. If your dynamic creative work has been theoretical because of latency budgets — and for most B2B advertisers I speak to, it has been — that excuse is dissolving. Have the conversation between your creative team and your media team about what reactive, signal-driven, individual-level creative could actually look like for your accounts. The infrastructure is catching up to the ambition that has been on B2B marketing whiteboards for five years.

Fourth, watch ARTF and AAMP at IAB Tech Lab. This will determine whether containerisation becomes an open-web pattern with multiple exchanges, multiple bidders and genuine interoperability — or whether it consolidates into one or two vendor ecosystems with switching costs. The market structure outcome here matters more than which specific platform wins the first phase, and AAMP is the upstream layer that will define how AI buying agents interact with that infrastructure.

Fifth, reassess the build-versus-buy framing for your programmatic capability. The cost calculus that justified building or acquiring in-house DSP capability between 2017 and 2022 has fundamentally changed. The reasons most holdcos and adtech players gave for owning a DSP — control of the bid, ownership of the data, capture of the margin — can now be achieved without the infrastructure burden. Specialist managed service running on containerised infrastructure is structurally cheaper to operate than in-housed mid-tier DSP capability, and the gap is going to widen rather than narrow. Microsoft just shut down the most credible mid-tier DSP in the market. The rest of the mid-tier doesn’t have Microsoft’s balance sheet.

A practitioner’s read

The fifteen-year DSP land grab was an accident of the cloud-cost paradigm, not a feature of how programmatic was meant to work. When the constraint goes, the orthodoxy that grew up around it goes too. For B2B programmatic — where the audiences are smallest, the inventory most fragmented, the cost of guessing largest and the demand for impression-level intelligence highest — this is the most consequential infrastructure shift since the transition from waterfall to header bidding a decade ago.

The next twelve months will be defined by two divergent answers to the same question. Microsoft’s answer is to consolidate into AI-mediated buying inside a walled garden. Index and Bedrock’s answer is to rebuild the open web’s economics so that specialists can compete at scale. The first will determine where some of the biggest advertisers spend their money. The second will determine whether the open web remains the place where B2B advertisers — who don’t have a walled garden of their own to retreat into — can find the audiences they need.

For B2B marketing teams the practical implication is that the kind of campaign you have been told was possible but couldn’t quite be delivered — true reactive creative, person-level buying committee personalisation, real-time signal integration into live media — is moving from pitch deck to production. The platforms that get there first will be the platforms that already had specialist B2B capability and moved early on the containerised architecture. The platforms that don’t will be explaining why their numbers have stopped improving.

The B2B Stack is written by Mike Harty, co-founder of FunnelFuel.io, a B2B-native programmatic managed service operating across London, New York and Singapore. If you’d like to talk through what this shift means for a specific ABM programme, named-account strategy or in-flight stack architecture, reply to the email or message me on LinkedIn.