The Ultimate 2026 Guide to B2B Programmatic Advertising: The Full Stack, The Real Gaps, and How to Win Multi-Channel

A back-to-basics, no-bullshit reference for B2B marketers, agencies, and operators running programmatic

Most “programmatic for B2B” guides you’ll read in 2026 were written by someone who has never bought a deal ID, never negotiated a curation fee, and couldn’t tell you the difference between SupplyChain Object validation and a seller-defined audience if you put a gun to their head. If this sounds like made up nonsense, read on!

That’s not a dig. It’s the structural reality of B2B marketing content. The people who write about this stack for a living are mostly not the people who operate it. The result is an infinite library of 1,500-word blog posts that describe programmatic the way an in-flight magazine describes turbulence — with more enthusiasm than understanding.

This guide is different because it has to be. I’ve spent fifteen-plus years inside this space — native advertising before it had a name, B2B programmatic before anyone thought to call it that, and now running FunnelFuel, a B2B-native programmatic managed service operating across London, New York and Singapore. What follows is an operator’s view of the 2026 stack: how it actually works, where the money flows, what’s genuinely new, and, most importantly, where it quietly breaks when you try to run B2B through infrastructure that was built for B2C.

If you’re in-housing paid media at a B2B SaaS, running accounts at a B2B agency, or trying to decide whether your current stack is fit for the pipeline numbers on your 2026 plan, this is the full-stack reference to bookmark.

What we’ll cover:

The anatomy of the modern programmatic stack — the six layers that actually matter.

How SSPs and DSPs have converged, and what that means for margin and control.

Identity in 2026: cookies aren’t dead, but they also aren’t reliable. What is the solution?

Data at segment level: firmographic vs behavioural, and where the wiring breaks.

First-party data as a compound-interest asset — not a one-time activation.

Where real innovation is happening — curation, AI optimisation, new channels, and the OpenAI question.

The seven places the whole thing breaks when you try to run B2B through it.

The best platforms for B2B brands, honestly assessed.

Why the best in-house teams still work with best-in-class managed service — and what “best-in-class” actually means.

Part 1: The Anatomy of the Modern Programmatic Stack

Forget the Lumascape. It’s a useful artefact of ecosystem complexity but a bad frame for understanding what’s happening when a B2B ad serves in 2026.

The stack you need to understand has six layers.

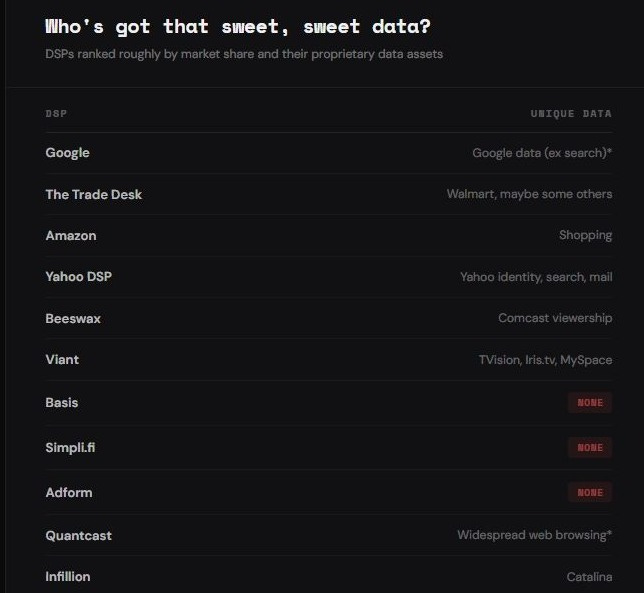

1. Demand side. The DSP (Demand-Side Platform) — The Trade Desk, DV360, StackAdapt, Amazon DSP, Yahoo, Basis. This is where campaigns are built, bids are placed, and optimisation happens. Traditionally competed around strength of inventory access, now more differentiated around unique data sets and capabilities.

2. Supply side. The SSPs (Supply-Side Platforms) — Index Exchange, Magnite, PubMatic, OpenX, Xandr — aggregate publisher inventory and sell it to DSPs via real-time auction or private deal. Evolving towards DSP-lite capabilities and shaping of inventory via curation.

3. Identity and matching. The plumbing that lets a DSP bid on an impression it can actually value. Universal IDs (UID2, ID5), hashed email matching, seller-defined audiences, IP-based identity, device graphs, CTV ACR. The technology architecture which enables data (see below) as well as frequency management and other programmatic bidding and pacing tooling

4. Data. Audience segments, intent signals, firmographic and technographic overlays. The B2B-relevant sources: Bombora, LinkedIn, Dun & Bradstreet, TechTarget, G2, 6sense. The ability to understand the user behind the ad opportunity, and shape bidding, creative and reporting capabilities. Mainly comes in the form of first party data (your own, such as your customers emails) or third party (somebody else’s data, like Bombora).

5. Measurement and attribution. What did the campaign actually do? This is the layer that most quietly hurts B2B marketers — we’ll come back to it.

6. Creative and activation. Dynamic creative optimisation (DCO), display and native formats, CTV, audio, DOOH, in-app. The message that we put in front of the user who we’re targeting

In a simplified buy, the DSP evaluates an impression offered by an SSP, checks whether it matches the campaign’s targeting (identity + data), places a bid in a fraction of a second, wins or loses the auction, and serves creative. The measurement stack then tries to tell you whether any of it worked.

The structural problem for B2B is that every one of these layers was designed to optimise for B2C outcomes, and against a single user based data hierarchy - which does not understand buying committees and accounts. We’ll spend most of this guide on what that means in practice.

Part 2: The Great Convergence — SSPs and DSPs Are Eating Each Other

The tidy separation between “sell side” and “buy side” that defined the Lumascape era is gone. What’s happening in 2026 is convergence, and it has real consequences for where margin sits and how you should think about supply.

On the demand side, The Trade Desk’s OpenPath (launched in 2022) established the direct-to-publisher model for DSPs. In early 2026, TTD expanded this with OpenAds — a next-generation auction platform with publisher commitments from AccuWeather, BuzzFeed, the Guardian and Hearst, among others. The thesis is straightforward: cut SSP take rates out of the path, win more auctions at a lower net cost. Yahoo’s Backstage initiative and Amazon’s Publisher Direct are versions of the same play. The argument extends to the commoditisation of supply - the same publisher will sell their inventory via header bidding via dozens of SSPs. Therefore, the DSP knows they gain a cleaner view of supply without the re-selling and duplication when they connect directly with the worlds best publishers.

On the supply side, SSPs are going buy-side as part of their counter-attack against DSP’s treading on their toes. PubMatic Activate lets advertisers execute direct campaigns through the SSP. Similar capabilities are being rolled out across Magnite and Index. Equativ will give you access to their DSP with a 0% fee when you buy their inventory. The boundary is dissolving.

The endpoint most people in the ecosystem now see coming is the UAP — the Unified Ad Platform — a single system that manages audience, bidding, yield, and inventory across the entire supply chain. We’re not there yet. But the direction is real, and it matters for B2B specifically because:

Shorter supply paths mean better economics. Fewer middlemen, lower take rates, more of your budget reaching the publisher.

But they also mean more concentration. When one DSP controls both the bidding and the publisher relationship, you have a single point of negotiation and a single point of failure. In reality you have that with the existing system anyway, because if your DSP falls over, you probably can’t reach your supply today anyway - but it is still worth flagging

Curation is where the action is. The real locus of value creation in 2026 isn’t the pipe — it’s the audience container that sits on top of it. The deal ID is the new unit of strategy and expect it to get superseded with audience containerisation and bidders (most likely leightweight ones taking advantage of curations power) to start to live IN the containers, essentially creating a UAP. This is a very hot area of innovation

Which brings us to identity.

Part 3: Identity in 2026 — Cookies Aren’t Dead, But They Also Aren’t Reliable

The programmatic ecosystem was architected around third party cookies. They acted as a store of data, enabling DSPs and SSPs to ‘cookie-sync’, allowing the DSP to make more of the SSP’s inventory ‘addressable’ - meaning the DSP could unlock the data it had on each user in the supply ecosystem. This is critical to audience intelligence but also to fundamental DSP capabilities, like frequency management (capping impressions at, for example, a maximum of 5 per user). So the outcry around cookies falling off a clifftop was huge, and consumed the messaging around programmatic for most of the early 2020’s.

In July 2024, Google abandoned its plan to deprecate third-party cookies in Chrome. In 2026, the live state is a “Privacy Choice” prompt that lets users decide — rather than Google deciding for them.

This surprised people who were expecting a cliff. What actually happened was a slow erosion. Safari (Intelligent Tracking Protection) and Firefox (Enhanced Tracking Protection) have blocked third-party cookies by default for years. Combined with ad blockers, cookie-consent opt-outs, and user privacy behaviour, a substantial share of the open web is either cookieless or flagged as low-signal before an auction even starts.

The working identity stack in 2026 looks like this:

Universal IDs. UID2 (The Trade Desk’s open standard, widely adopted), ID5, LiveRamp’s RampID. These are mostly hashed-email-based deterministic identifiers that work in places where cookies don’t. ID5 is more probabilistic and behaves a little bit differently

Seller-defined audiences. IAB’s standard that lets publishers expose audience signals directly, bypassing the identity layer entirely for some use cases.

Contextual and semantic targeting. Not identity at all, but increasingly sophisticated thanks to AI: topic taxonomy, content-level matching, LLM-driven semantic relevance.

Device graphs and probabilistic matching. For CTV, mobile app, and cross-device stitching where deterministic IDs aren’t available.

For B2B specifically, identity is where the stack starts to wobble. All the universal ID infrastructure is built around consumer email matching. Consumer email is simply a much more persistent signal - you may have your old Gmail from 15 years ago, you probably do not have your work email from 15 years ago. The moment you try to ask “is this impression being served to someone at a target account?” you’re asking a question the universal ID framework doesn’t natively answer.

We’ll come back to this in Part 7. It’s the single most important thing B2B marketers misunderstand about their own stack.

Part 4: Data at Segment Level — Where the Real Margin Leaks

Every B2B media plan in 2026 leans on third-party data segments. Here’s what actually happens when you activate one.

The segment is created by ant one of the plethora of data providers — which could be Bombora for intent, D&B for firmographics, TechTarget for technographics, 6sense and Demandbase for buying-stage signals. That segment is matched (typically via cookie ID, UID2, or IP) to users or devices. The matched segment is packaged into a taxonomy and distributed to DSPs. You target it.

Each step loses signal.

Match rates degrade. A segment claiming two million accounts in its source data might match 15–30% of that when activated against open-web impression supply. Fewer in cookieless environments.

Data decay. Intent signal is freshest on day one. By the time it’s flowed through the taxonomy, matched, and hit your DSP, you’re often operating on one- to two-week-old signal. For fast-moving B2B cycles, that’s material.

Segment aggregation. Most commercial B2B segments are aggregated at person or household level, then inferred back up to account level. That inference is where a lot of precision dies.

Hierarchy mismatches. If you target “IT Decision Makers at Fortune 500 companies,” the segment is built by joining signals that were never deterministically linked. You’re buying an inference, not a matched audience.

The other huge issue with segments is that you can only target and report at a segment level - and a segment may = 10,000 accounts. So all you get back is impressions, clicks etc at a 10,000 account segment level. No account level data. No ability to shape your bids to match surging engagement or other buying signals coming out of your CRM. This is the problem that has only really been solved by IABM from TradeDesk, Bombora and ChaliceAI, and FunnelFuel (built into SSPs and DSPs as adtech upgrade package for B2B)

The operator move is to treat third-party segments as a directional tool, not a ground truth, and to prioritise paths where the signal is closer to source. That means:

Direct relationships with data providers where possible. Raw signal access beats pre-packaged segments.

Curated deal IDs that align inventory, context, and audience in one package. The Audigent, D&B, and Experian curation stacks are instructive. Over 400 Dun & Bradstreet B2B audience segments are now activatable via Audigent-curated deal IDs across CTV, display, native, audio, and online video.

First-party data layered on top of third-party segments, not replaced by them.

Which brings us to the compound-interest play most B2B marketers still under-index on.

Part 5: First-Party Data — The Asset You Actually Own

If you take one thing from this guide: the B2B marketers winning in 2026 are the ones who have built first-party data into the core of their programmatic activation, not bolted it on as an afterthought.

Third-party data is rented. It’s degrading. It’s increasingly expensive, matched to shrinking pools of addressable users. The quality cannot easily be audited and the segment owners are incentivised by their cost per thousand revenue model, to inflate the segment size. First-party data is the opposite on every dimension. It compounds, it’s owned, and match rates to your own CRM and MAP are structurally higher than anything you’ll ever buy.

The B2B first-party data playbook in 2026:

1. Build the pipes first. Your CRM (Salesforce, HubSpot, Dynamics) and MAP (Marketo, HubSpot, Pardot) are the source of truth. Get the identity graph clean before you try to activate any of it. Hashed emails, IP data, form-fill metadata, LinkedIn unique IDs, D-U-N-S numbers — these are your activation tokens.

2. Segment by intent stage, not just ICP. Early-stage research visitors behave differently from BDR-engaged accounts, which behave differently from late-stage opportunities. Build segments that match how your pipeline actually moves, then activate each with a different media strategy.

3. Activate through multiple surfaces. Customer match in programmatic and LinkedIn is the obvious layer. Less obvious but more powerful: activating hashed CRM records directly into the DSP, matching them via UID2 or IP-based identity, and using them as targeting seeds or suppression lists across your full media mix.

4. Measure back to source. Every first-party activation should close the loop into your CRM. Exposed accounts, engagement scores, pipeline progression — all of it should live in the system the sales team already looks at.

This is where B2B-native measurement earns its keep. We’ll get to that in Part 7.

Part 6: Where the Innovation Is Actually Happening

A lot of what gets sold as innovation in B2B adtech is features dressed up as revolutions. Here’s what’s actually moving in 2026.

Curation and audience containers

The single biggest shift in how media is bought and sold is curation. Experian’s 2026 State of Advertising report makes the case plainly: programmatic is shifting from broad open-exchange access to curated, performance-ready supply paths.

For B2B, this matters because curation is finally solving a problem that open-exchange programmatic has always had: matching the right firmographic audience to the right contextual environment at the right price, in a way that a self-serve DSP seat simply cannot.

Curators like Audigent, Experian, and specialist B2B operators are building audience containers — curated deal IDs — that combine vetted inventory, joined data, and margin protection in a single activation token. The advertiser buys the deal ID; everything underneath is pre-negotiated.

The strategic implication: in 2026, if you’re running B2B programmatic at any scale and you’re not operating through curated deal IDs, you’re leaving both performance and margin on the table.

AI optimisation — the real version

Every DSP has been calling everything AI for five years. What’s actually new in 2026:

Bid-level optimisation models that learn auction-by-auction rather than campaign-by-campaign, materially reducing wasted impressions on B2B activations.

Creative optimisation — LLM-assisted DCO that adapts copy to buying stage, firmographic segment, or account intent level.

Semantic context matching — moving beyond keyword-and-category contextual targeting to LLM-evaluated page content. This is dramatically better for B2B, where relevant context is often nuanced (”a CFO article about working capital cycles,” not “finance vertical”).

Audience expansion and lookalike modelling on first-party seeds — genuinely useful now that the models can operate on structured firmographic dimensions rather than just behavioural ones.

The test for any AI feature: does it demonstrably reduce waste or improve outcomes against a first-party-measured baseline? If it doesn’t, it’s a pitch deck.

Formats and channels

CTV is now fully programmatic and fully relevant to B2B — the “B2B decision-makers watch CTV too” argument has won and paid search money is moving over on mass. DOOH has become more targetable via data-linked screens, especially in business districts, and ABM versions of it can now be run globally. Audio — podcast advertising, Spotify DSP inventory — continues to grow, and is probably the single most under-represented audience pool considering the latest stats show that ITDM’s spend upwards of 54 minutes a day on podcasts. Retail media, which has dominated the B2C conversation for three years, is still mostly irrelevant for B2B unless you’re selling into commerce.

The interesting wildcard is CTV plus account targeting. This is hard — CTV identity is usually household- or device-based rather than person-based — but curation stacks combining IP-based account identity with CTV supply are making genuine account-level CTV targeting viable for the first time. Campaigns are showing incredible promise for B2B lead generation when optimised against attention metrics

The OpenAI question — and the new conversational surfaces

The event that every B2B marketer should be paying attention to: OpenAI launched paid advertising in ChatGPT on January 16, 2026, initially on Free and Go tier users in the US. The entry threshold is enterprise-grade — reported at roughly $200,000 committed beta spend — and Criteo became the first adtech integration partner in March 2026. Google has committed to bringing ads to Gemini in 2026. Perplexity has been building sponsored content for some time.

What this means for B2B: a new set of conversational AI surfaces is becoming an advertising channel, and the first movers will learn more about how to use them than anyone can extract from case studies later. For B2B specifically, these surfaces are particularly interesting because they intercept intent at the research stage — exactly when the buying committee is forming its options. And we know upwards of 90% of B2B buying journeys are now shaped or at least influenced by LLM ‘co-pilots’

None of this is ready for primary spend in 2026. But it’s ready for structured experimentation, and the marketers who will have an advantage in 2027 are building their testing programs now.

Part 7: Where the Whole Thing Breaks for B2B

This is the section most “programmatic for B2B” guides never write, because writing it requires admitting that the infrastructure is mostly not built for the job you’re doing.

This is why I theorised in late 2020 that the worlds best adtech needed an ‘upgrade pack’ - a tech layer that would upskill its capabilities for B2B WITHOUT building a homebrew DSP. The wheels and engine didn’t need re-building but the data models sure did. Anyone trying to run programmatic B2B will be familiar with the below challenges

1. No native account understanding. Every mainstream DSP operates natively on person, device, or household as the unit of targeting. Account is a derived layer, not a native one. When you target “IBM” in your DSP, what’s really happening is pattern-matching of IPs, known personas, and firmographic-tagged identifiers — with all the noise that implies.

2. Buying committees are invisible to the stack. B2B purchases are made by committees of six to ten people. A programmatic stack that optimises for individual-level engagement will systematically under-value the multi-touch, multi-person pattern that actually indicates pipeline movement. Most platforms cannot tell you that five different people at a target account engaged with your brand in the last 30 days — because they were never built to care about that.

3. Data hierarchy mismatches. Third-party B2B segments are built in a B2C taxonomy and retrofitted. The decision-tree logic (”IT Decision Maker at 1000+ employee company in Finance”) sits on top of consumer-identity infrastructure that wasn’t built to carry firmographic weight. Activation works; precision is largely theatrical.

4. Segment-level scale gaps. Commercial B2B segments lose 50–70% of their inferred scale between source and DSP activation once you account for match rates, freshness decay, and unique-user deduplication. The numbers on the rate card are almost never the numbers that reach impression delivery.

5. Reporting on delivery, not account progression. The DSP will happily report impressions, clicks, CTR, viewability, and CPM. It will not tell you which target accounts are more engaged this month than last, which have moved from cold to research stage, or which are showing buying-committee patterns. That’s the report B2B marketers actually need. Almost no platform produces it natively.

6. Attribution designed for last-click B2C. Most DSP attribution is a variant of last-click or probabilistic multi-touch. For a B2B buyer with a six-month sales cycle, that’s close to useless. Without offline conversion import, CRM integration, and account-level modelling, you’ll spend 2026 optimising against signals that don’t correlate with pipeline.

7. The margin stack is hidden. Between DSP seat fees, SSP take rates, data costs, curator margins, verification fees, and any agency or managed-service layer, the real working-media rate on a typical B2B campaign is often 40–60% of gross spend. Most in-house teams don’t know their own number. The ones that do win the budget arguments.

This list isn’t a pitch for any particular solution. It’s the structural reality of running B2B through infrastructure that wasn’t built for it. Once you see it clearly, you stop asking “how do we do programmatic better?” and start asking “how do we build around these gaps?”

Part 8: The Best Platforms for B2B Brands in 2026

There is no single best platform. There are platforms that solve specific parts of the B2B problem, and the art is assembling the right combination. An honest tour:

DSPs worth knowing

The Trade Desk. The best independent DSP. Deep supply relationships, OpenPath and OpenAds direct-to-publisher access, strong identity infrastructure (UID2), genuinely programmatic CTV, solid measurement API. Weak on native account-level reporting without an overlay.

DV360. Scale, YouTube integration, Google’s identity graph. Data operations are increasingly walled. Fine for B2B if you’re willing to accept Google’s measurement worldview as ground truth.

StackAdapt. Strong self-serve, good display and native, increasingly competitive CTV. Popular with agencies and mid-market B2B. Less deep on enterprise data integrations.

Amazon DSP. Unique data asset via Amazon’s retail graph. Relevant for B2B companies selling into commerce or with distributed supply chains. Niche otherwise.

B2B-specialised ABM platforms

6sense and Demandbase. The incumbents. Both offer integrated intent data, account identification, and media activation. Powerful, expensive, and often positioned as replacements for a full stack when they’re really one layer within one. Media delivery is rarely best-in-class even when the signal layer is strong.

RollWorks. Solid mid-market ABM, good pipeline integration.

Terminus. Continues to evolve; historically strong on ABM orchestration.

Metadata. AI-driven campaign automation. Useful for smaller teams without in-house media operators.

Influ2. Person-based advertising; narrow but differentiated niche.

The honest reality: no single one of these platforms solves the full B2B programmatic problem end-to-end. The ABM platforms give you account signal but constrain your media surface. The DSPs give you media surface but can’t give you account-level reporting natively. The gap between them is where most B2B marketers quietly burn budget.

Part 9: Why the Best In-House Teams Still Work With Managed Service

Here’s a pattern I’ve watched for 15 years — and especially sharply for the last five: the smartest, best-resourced in-house B2B marketing teams don’t move to full in-housing for programmatic. They in-house the strategy, the brand, the planning, and the measurement — and they work with a best-in-class managed service for the execution layer.

This is counter-intuitive if you’ve read the consultancy pitches that frame in-housing as primarily a cost-saving exercise. It makes sense the moment you look at what “managed service done properly” actually delivers.

1. Access, not outsourcing. The right managed service partner isn’t renting you a trader. They’re giving you access to supply relationships, curated deal IDs, raw data partnerships, and tech integrations that an in-house team — no matter how well-funded — cannot economically replicate. Raw signal-level data access (the kind FunnelFuel built with Bombora as only the second company to hold that level of integration) is the clearest example, but it’s not the only one. Supply-side relationships, curation stacks, and first-look deal pipelines are all asymmetric assets that a managed service can offer structurally.

2. Expertise that compounds across clients. A managed service working across dozens of B2B campaigns sees patterns an in-house team running only its own activity never can. What works for a cybersecurity vendor informs what works for a fintech, which informs what works for a SaaS marketing platform. That cross-sectional pattern recognition is impossible to recreate internally.

3. Margin protection through scale. Managed services that operate on the supply side — curating their own deal IDs, negotiating directly with SSPs, holding raw data partnerships — can deliver working-media rates that an in-house team cannot match at typical scale. The case for in-housing almost always assumes the in-house team can operate at specialist margins. It almost never can.

4. Account-level measurement as default. A B2B-native managed service builds the HVA scoring, the account progression reporting, the buying-committee detection — because that’s the job. A DSP seat gives you impressions; a managed service gives you a pipeline story.

5. Focus. An in-house team’s “programmatic specialist” is usually also their email specialist, their paid social strategist, and their webinar operator. A dedicated B2B programmatic partner has one job and does it across their waking hours.

The litmus test: does your managed service get you results, measurement, and access that you provably cannot replicate in-house at the same cost? If yes, it’s not a cost — it’s a capability. If no, it’s a cost, and you’re right to in-house.

The 2026 B2B Programmatic Scorecard

Seven questions to ask against your own stack:

Supply path. Are we buying through curated deal IDs, or mainly through open exchange?

Identity. Do we have a working first-party identity graph, and are we activating it programmatically?

Data. Do we have direct or raw-signal access to the data providers that matter for us, or are we buying pre-packaged segments through three layers of resale?

Measurement. Can we report on account progression, not just delivery?

Channel mix. Are we running multi-channel (display, CTV, native, audio) from a single orchestrated plan, or stitching together disconnected activations?

Innovation surface. Are we running structured experiments on emergent surfaces — curation innovations, AI optimisation features, ChatGPT/Gemini advertising — or waiting for them to become proven?

Margin. Do we know our true working-media rate after all fees, and is anyone held accountable for improving it?

Clean answers to all seven puts you ahead of 95% of B2B brands. If you don’t have them, that’s the honest gap analysis — and it’s where 2026 budget should go first. Hit reply to this email if you need help going through any of this

Where This Leaves You

Programmatic in 2026 is more powerful than it’s ever been and more dangerous to run on autopilot than it’s ever been. The stack has converged, matured, and specialised simultaneously. The gap between B2B marketers who operate it intentionally and B2B marketers who let their DSP seat run on defaults has never been wider — and it will widen further as AI optimisation, curation, and emergent channels like ChatGPT ads pull the front of the pack further ahead.

The point isn’t that programmatic is hard. It’s that programmatic for B2B is specifically hard, because the infrastructure isn’t natively built for the job. The marketers who win in 2026 aren’t the ones with the best DSP seat. They’re the ones who understand the gaps clearly enough to build around them — and who partner with the people who’ve already built the scaffolding.

If you’re running B2B programmatic in-house and want to pressure-test your stack against what we’ve covered here — supply path, identity, data, measurement, margin — reply to this email. It comes straight to me and we can get into it. I read every response, and these conversations are usually the most interesting part of my week.

And if you want more of this — full-stack B2B adtech analysis, written by someone who’s actually operating the stack — you’re in the right place. Hit subscribe if you haven’t already, and forward this to the one person on your team who’d genuinely benefit from reading it.

Mike Harty is the founder of FunnelFuel, a B2B-native programmatic managed service operating across London, New York, and Singapore. The B2B Stack is his practitioner-led newsletter for B2B marketers, agencies, and operators working in programmatic.